Alex Tabarrok is convinced we’re at full employment:

To begin, full employment does not mean the lowest possible unemployment rate. We are at full employment when we are at the natural rate of unemployment… When the production of apples is bigger this year than last year we don’t jump to the conclusion that last year the apple market was out of equilibrium. Similarly, the fact that unemployment was lower this year than last year does not mean that we weren’t at full employment last year.

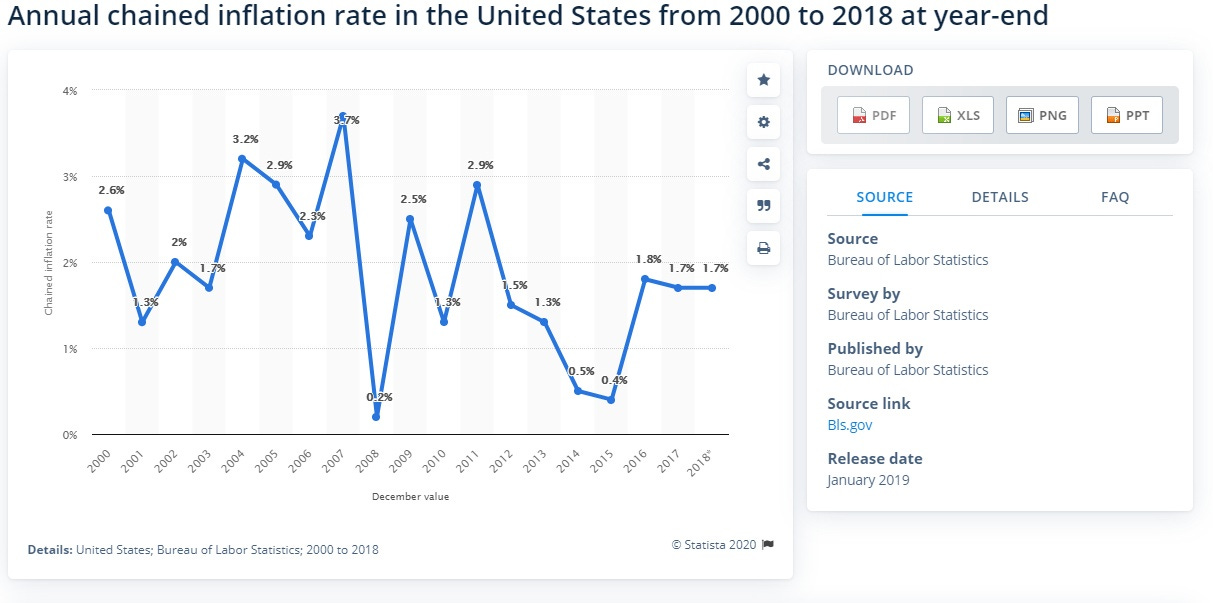

I’m not so sure. Perhaps the most informative alternate name for the “natural rate of unemployment” is the NAIRU – the Non-Accelerating-Inflation Rate of Unemployment. So if you see low, stable inflation, that could mean you’re at the natural rate. Or it could mean that you’re above it. So what’s been going on lately? This:

Quick version: Inflation has been low and stable for several years. This could mean we’re right at the sweet spot. The more likely scenario, though, is that we’re not quite there yet.

How can we ever find out? The only way to really know is to push our luck a little bit, make monetary policy more expansionary, and see if inflation starts to spiral upwards.

Is that wise? To be honest, I’m conflicted. I find the Akerlof-Dickens-Perry model, which features a long-run inflation-unemployment trade-off, to be quite convincing. I also buy the market monetarist view that a modestly higher inflation target – say 3% – would be a welcome buffer during the next recession. On the other hand, though, the 1970s showed that a casual attitude about inflation can get severely out of hand, leading to chronic stagflation and miserable disinflations.

All things considered, I’d stay the course. Yet if the Fed announced it was going to raise its target rate to 3%, I would not fret.

What I am confident of, though, is that economists are wrong to confidently assert that we’re already “at the natural rate.” Yeah, maybe we are. Still, there’s got to be at least a 30% chance that we remain, say, half a percentage-point above. Remember: If nominal wage rigidity is currently irrelevant in 90% of jobs, but remains a binding constraint in declining occupations and rural areas, then inflation still erodes nominal rigidity and increases overall employment. Is that really so hard to believe?

The post appeared first on Econlib.