What the Hell Is Going On With the Economy?

Cult classic The Room is quotable throughout, but over the last two years, I’ve kept coming back to, “People are very strange these days.” This is true in almost every area of life, but as I an economist I’m hyper-aware of a long list of weird economic patterns. To wit:

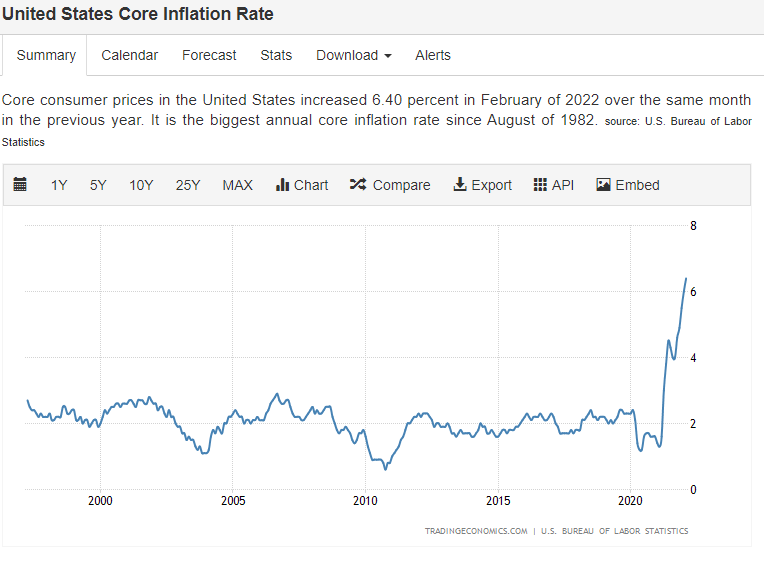

1. The highest inflation since my childhood, now at 8.5%. Despite the many excuses you’ve heard, most of this is not temporary supply shocks, but classic core inflation.

2. Lots of shortages, in the technical economic sense that I cannot obtain the quantities I want by paying the listed market price. This used to happen to me maybe once per month; now it happens about twenty times per month. Shortage goods I’ve experienced include: table service at P.F. Chang’s, chocolate chocolate chip ice cream, calamari, BBQ beef and pork, light bulbs, haircuts, home electronics installers, non-solidified Gorilla glue, and many more.

3. Quite a few items seem unavailable at any price, unless you have the right personal connections. A friend of mine who is building a new house can’t obtain garage doors or a heating oil drum.

4. Unemployment near its 50-year low of two years ago, after the largest unemployment spike in recorded U.S. history.

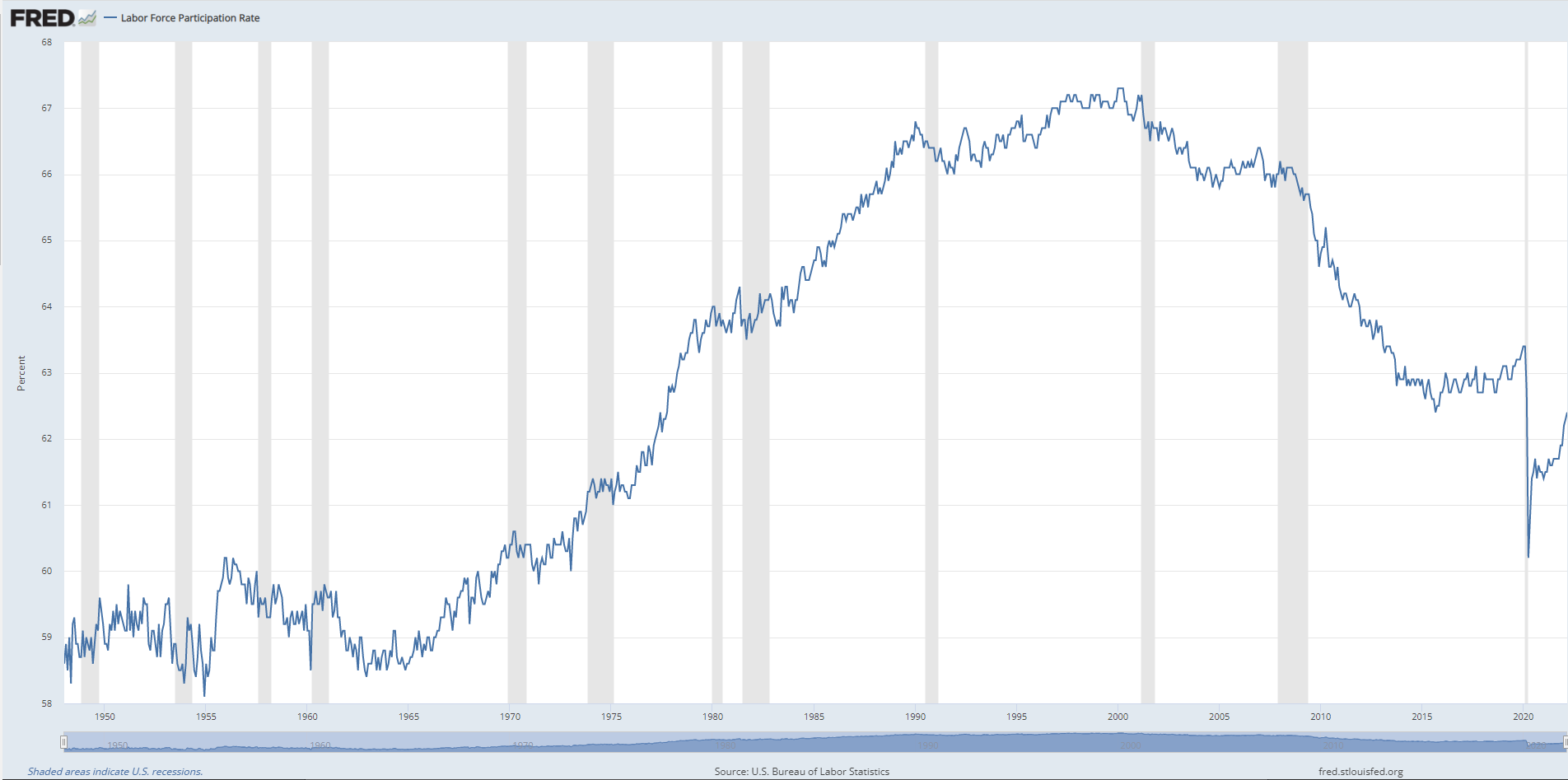

5. Labor force participation (LFP) still below the minimum for the late 1970s through March of 2020.

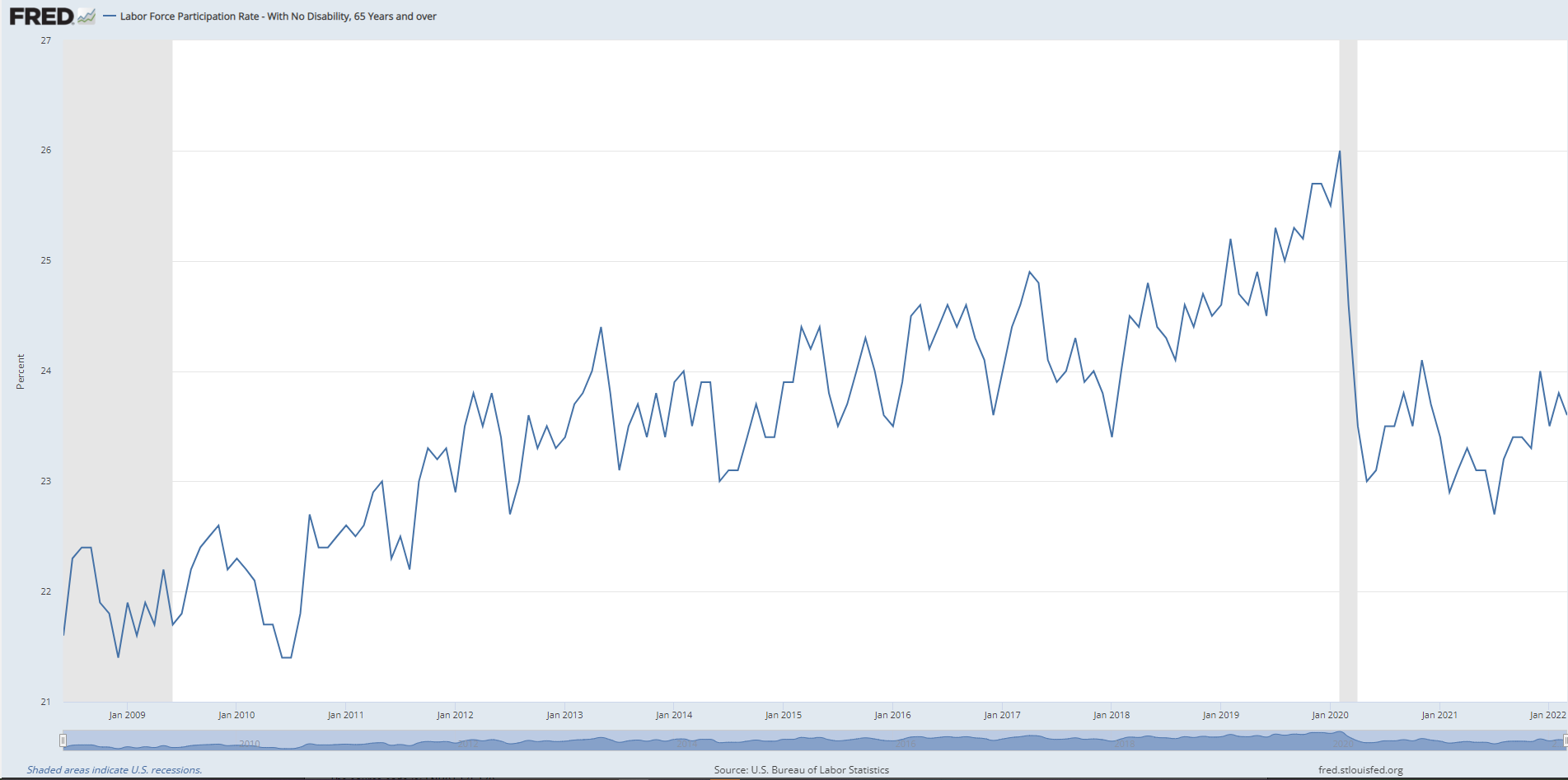

6. Near-full recovery of prime-age LFP, but less recovery for young workers, and a sharp reversal of historic trends for 65+ LFP.

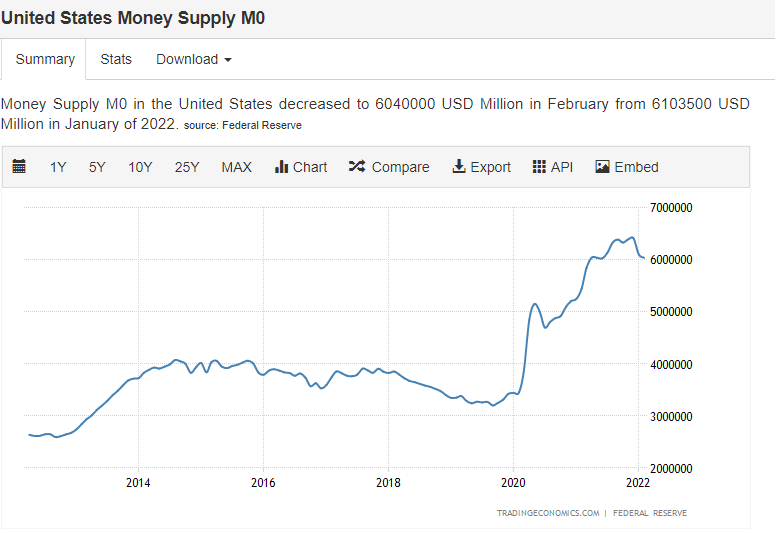

7. The Federal Reserve has been extremely accommodative even though the chair, Jerome Powell, is not only a Republican but a Trump nominee - and core inflation is triple its normal level. Yes, they’re finally contracting the money supply, but only mildly after a near-doubling.

Is this really all so strange? Yes! Most notably:

Expansionary fiscal and monetary policy are common during crises, but government normally compensates somewhat less than 100% for falling private demand - not markedly more than 100%.

When inflation is high, shortages (again, in the technical sense that you can’t buy all you want at the list price) normally do not become noticeable… unless the government imposes price controls as well.

LFP normally stays roughly on trend during recessions, consistent with the standard story that high unemployment reflects low Aggregate Demand, not low Aggregate Supply.

When core inflation gets high, the Fed normally deliberately creates a recession to counteract it. That’s the classic “Romer dummies” story.

So what the hell is going on? All of the following:

Fiscal policy absurdly overreacted. Not as extreme as the overreaction of Covid policy itself, but in the same innumerate and fanatical spirit.

The Fed embraced a wartime-level abandonment of central bank independence. Normally, if the Fed thinks that fiscal policy is overly loose, they make monetary policy offsettingly tight. But during wars - and now pandemics - they obediently print all the money necessary to prevent the standard effect of profligate borrowing. Namely: skyrocketing interest rates.

To see the severity of the Fed’s submission, just look at real interest rates. The inflation-adjusted prime rate is now about negative 5%.

Powell and other Republican central bankers have been severely alienated by Trumpian populism, just like most educated Republicans. As a result, the Fed is making a bipartisan decision to aid the Democrats by delaying the inflation-cutting recession until right after the 2022 midterm elections.

Widespread nominal fairness norms are holding many prices below the market-clearing level. Businesses are run by human beings, and the crisis mentality has been so severe that firms continue to charge prices not only (a) below the profit-maximizing level, but (b) below the level necessary to keep goods on the shelves. These norms mimic the textbook effects of mild price controls.

These nominal fairness norms, in turn, have caused secondary shortages in labor markets. Norms keep firms from raising prices, which makes it hard for them to afford to raise wages either.

You may be tempted to blame labor shortages on monopsony: Firms could make more profits by raising wages for new workers, but choose not to do so because this would force them to raise wages for old workers, too. Problem: If this is the right story, firms would rush to raise prices, because this would allow them to make more money on both new and old sales. The purely norm-driven story can explain both sluggish wages and sluggish prices; the monopsony story, in contrast, incorrectly predicts sluggish wages and vivacious prices.

As you’d expect, many older workers have retired early due to fear of Covid. Not so weird.

What is weird: Lots of younger workers have successfully used Covid to exit the workforce, too. Profligate Covid relief aside, quite a few parents who wouldn’t have tolerated young adult idleness relaxed their Puritanical attitudes for Covid, despite the very low risk for the young, and the ultra-low risk for the vaccinated young. Yes, it’s the macroeconomics of hypochondria. Though since prime-age adult LFP is almost normal, it looks like elders are mostly humoring the hypochondria of the young.

I know this all sounds a little ad hoc, but that’s my story.

P.S. Expect me at the April 16 midnight showing of The Room at DC’s E St. Cinema. If you attend, please say hi. I’m the guy with the glow-in-the-dark football.

The US economy it's turning Japanese, I think it's turning Japanese, I really think so.

"The highest inflation since my childhood, now at 8.5%. Despite the many excuses you’ve heard, most of this is not temporary supply shocks, but classic core inflation." Not "most", but a "combo". I Europe it´s 100% due to supply shocks, which adequately explains the lower inflation there.

https://marcusnunes.substack.com/p/the-age-of-inflation-again?s=w